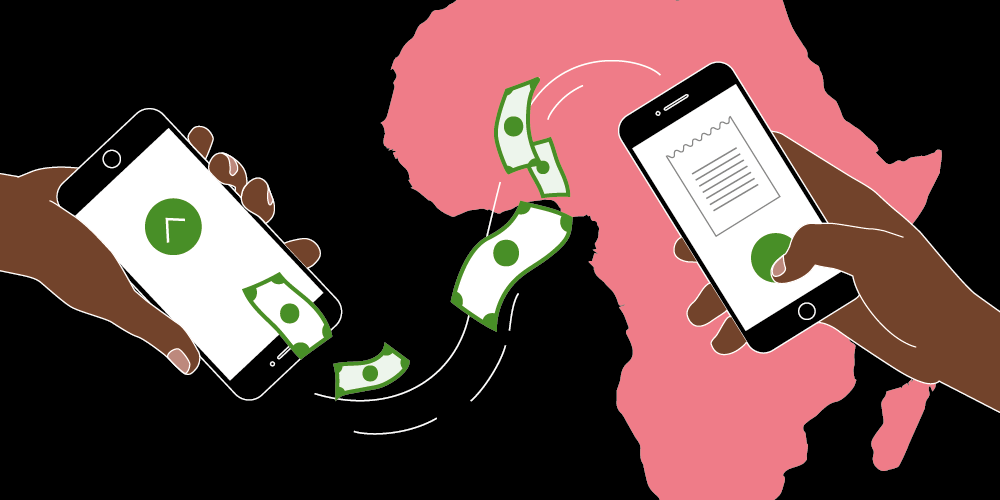

Today, being able to send and use money across different countries has become really important for businesses and regular people. However, in Africa, this simple task is full of challenges that can make it slow, costly, and very frustrating. From dealing with complex rules to outdated systems, the obstacles to easy cross-border payments in Africa are many.

Too Many Rules and Regulations

One of the biggest hurdles to smooth cross-border payments in Africa is the mess of regulations that govern financial transactions across the continent’s 54 countries. Each nation has its own set of rules, requirements, and authorities in charge, creating a maze of paperwork that can be hard to navigate.

For businesses operating in multiple African nations, this tangle of rules can be a nightmare. Understanding the different reporting needs, limits on money movements, and anti-money laundering protocols can be a huge time and money drain. Even for individuals sending money to family or making basic payments, the regulatory landscape can be intimidating.

Old Systems and Limited Access

On top of the regulatory challenges, Africa also struggles with outdated financial infrastructure and limited access to banking services, especially in rural areas. Many regions lack reliable internet and modern payment systems, making it difficult to do electronic transactions smoothly.

For those without access to traditional banking, the challenges are even bigger. Cash-based economies and reliance on informal money transfer methods, like hawala, can make cross-border payments a complex and unclear process.

High Fees and Currency Swings

Another major obstacle to cross-border payments in Africa is the high costs involved with these transactions. Banks and money transfer companies often charge very high fees, eating into the already limited financial resources of individuals and businesses.

Additionally, the constant ups and downs of African currencies can further complicate matters. Changes in exchange rates can reduce the value of money being sent or make it hard to accurately predict the cost of international transactions, adding uncertainty to an already complex process.

Trust and Security Worries

In an environment where financial infrastructure is often outdated and regulatory oversight can be inconsistent, trust and security concerns can also hinder cross-border payments in Africa. Fears about fraud, cybercrime, and the potential for money laundering can make individuals and businesses hesitant to engage in cross-border transactions.

Building trust in the systems and institutions that facilitate these payments is crucial, but it can be a challenging task in a region where financial services have historically been unreliable or inaccessible to many.

New Solutions on the Way

Despite these many challenges, there is hope on the horizon. Financial technology companies and other innovative players like HIZO are working to address the hurdles of cross-border payments in Africa, using new technologies and business models to create more efficient, secure, and cost-effective solutions.

HIZO, for example, is becoming very popular, providing a convenient and accessible way for individuals to send and receive funds across borders. Blockchain and cryptocurrency solutions are also being explored as potential alternatives to traditional payment systems, offering greater transparency and security.

Additionally, efforts are underway to make regulations more uniform and improve financial infrastructure across the continent, with initiatives like the African Continental Free Trade Area (AfCFTA) aiming to make cross-border trade and payments easier.